Luscid | 11 May, 2026

Why certain environments keep attracting the crypto category

A category that depends on context

Sponsorship has traditionally been used to build visibility. In many categories, repeated exposure is often enough to create familiarity and, over time, preference.

Crypto does not operate under those conditions.

Adoption requires more than awareness. It asks people to engage with financial systems they may not fully understand, accept a degree of volatility, and place trust in platforms that are still evolving. The decision is not simply whether a brand is recognised, but whether the category itself feels credible, relevant, and worth engaging with.

This is what makes sponsorship particularly important for crypto brands. Not as a shortcut to attention, but as a way of shaping context. Where a brand appears influences how it is interpreted. In a category where perception is still being formed, that context carries significant weight.

The audience is already closer than it looks

The environments crypto brands are drawn to are not arbitrary. They tend to attract audiences that already exhibit behaviours aligned with the category.

GWI data highlights that 62% of cryptocurrency investors have an interest in watching sport – a figure reflected through in the most recent Luscid report generated for the category. When scale of audience is the prominent driver – 8 of the top 10 passion points for a global cryptocurrency audience are sports.

Taking a closer look at some of the largest sporting properties, this scale is ever more apparent. U.S. World Cup audiences are significantly more likely to show interest in both cryptocurrency and financial markets more broadly, with 78% and 55% respectively (GWI, Nielsen). These are not just large audiences. They are audiences that are already comfortable with digital systems, financial experimentation, and performance-driven thinking.

This alignment reduces the distance a brand needs to travel to become relevant.

Formula 1 offers a clear example of this dynamic. The sport’s recent audience growth has been driven by younger, more globally distributed fans, particularly in the U.S., and increasingly among women (Formula 1). The result is a fan base that is more digitally native, more internationally connected, and more culturally fluid than in previous eras.

In that context, Formula 1 offers more than prestige. It provides access to an audience that crypto brands are actively trying to integrate into.

Investment is uneven, but still persistent

At a headline level, crypto sponsorship activity can appear volatile. Total deal value declined by 30% in 2025, a figure that could easily be interpreted as a retreat from the category (Luscid).

A closer look tells a different story.

According to Luscid, in 2024, total new sponsorship spend reached $312.9 million, but over a quarter of that came from a single brand. When that same brand reduced its activity dramatically the following year, overall deal value dropped accordingly. Yet even with that reduction, the sector still delivered $222 million in new partnerships in 2025. By the beginning of 2026, activity had already started to pick up again.

This is not a category disappearing. It is a category whose investment patterns are influenced by a small number of large players, but where underlying demand remains intact.

More importantly, that demand continues to concentrate in a relatively consistent set of environments.

Photo credits: Mark Sutton, 360 Magazine

Motorsport: framing crypto through performance

Motorsport has become one of the most prominent of those environments, and Luscid Brand Value Index data supports this trend. When Brand Synergy is the prominent factor in our cryptocurrency report, Formula 1 is the top passion point for a partnership solution with an index of 207.1, making it more than twice as powerful at delivering positive association with brand values relevant to the category.

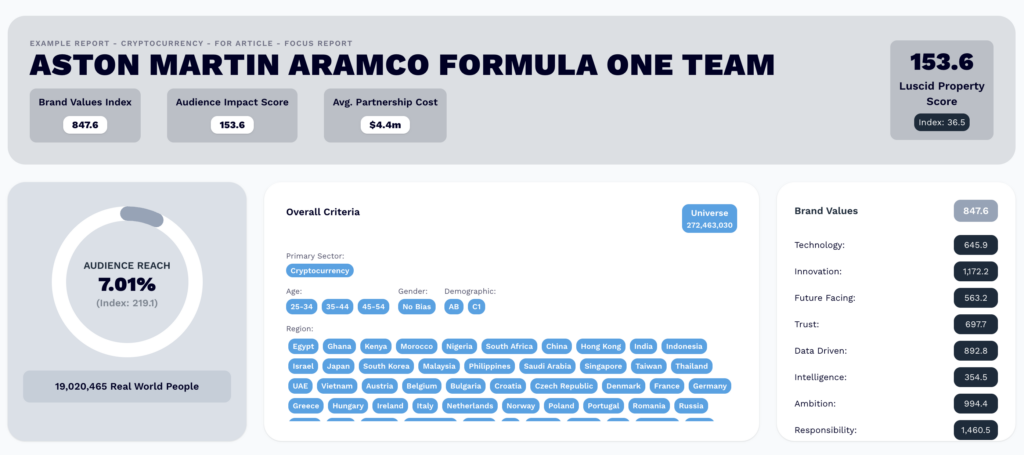

Long-term partnerships, such as Crypto.com’s relationship with Formula 1, and more structurally integrated deals like Coinbase’s partnership with Aston Martin, paid entirely in a stablecoin, signal a deeper level of alignment between category and platform (Formula 1; Coinbase).

On a team level, the Aston Martin deal is a fascinating case study. A property focus report built in Luscid against a global cryptocurrency user reveals that the team alone can reach 7% of this audience, which is twice the global individual average. From a brand value perspective, the index against positive sentiment association is 8.5x the global property average.

The scale of crypto’s presence in Formula 1 reinforces this insight. The category now accounts for 26% of the sport’s commercial ecosystem (up 70% YoY), with a growing proportion of financial partners coming from crypto and fintech (Business of Speed). Investment has surpassed the billion-dollar mark over recent years and continues to expand.

This concentration is not simply a function of visibility.

Motorsport operates within a framework defined by precision, speed, engineering, and financial intensity. These attributes mirror the way crypto brands want to be perceived: technical, high-performance, and embedded within systems that move at global scale.

Within this environment, crypto is not positioned as experimental. It is positioned as part of a broader performance economy.

Photo credits: Tullio Puglia, Action Images via Reuters

Football: turning presence into familiarity

If motorsport shapes perception, football performs a different function.

The category’s strong presence in football is driven by scale and frequency. Across 2025 and 2026 to date, 42% of all new crypto sponsorships were signed in football, including teams, leagues, venues and national federations (Luscid / Global Data). These are not just occasional placements, they are formats designed for constant visibility – with Sportquake insight highlighting 37% of all football deals featuring front of shirt or sleeve placements.

That logic is reflected in how partnerships are structured. Crypto.com’s agreement with the UEFA Champions League places the brand across broadcast, in-stadium and media environments at the highest level of club competition, while OKX’s Manchester City deal extends into training kit branding, sleeve rights and Web3-led fan experiences embedded in the club’s day-to-day ecosystem (UEFA; OKX).

Together, this creates a different type of impact. Football embeds brands into routine. Weekly fixtures, continuous broadcast cycles and global fan engagement ensure that exposure is not occasional but persistent, building familiarity through repetition rather than singular moments.

In this sense, football operates less as a signal of innovation and more as a distribution system. It allows crypto brands to move from being seen occasionally to being seen everywhere, accelerating recognition and normalisation across markets.

Photo credits: UFC, Reuters

Beyond the core: attention and context

Other sports show how the category adapts to different audience environments. Crypto.com’s long-term partnership with UFC, reportedly worth around $175M, places the brand at the centre of one of the most intense, high-attention sports ecosystems (UFC). As the organisation’s first global fight kit partner, the brand is embedded directly into the action, supported by activations such as fighter bonuses paid in crypto and integration across UFC’s digital content. The result is an environment where engagement is immediate and attention is highly concentrated.

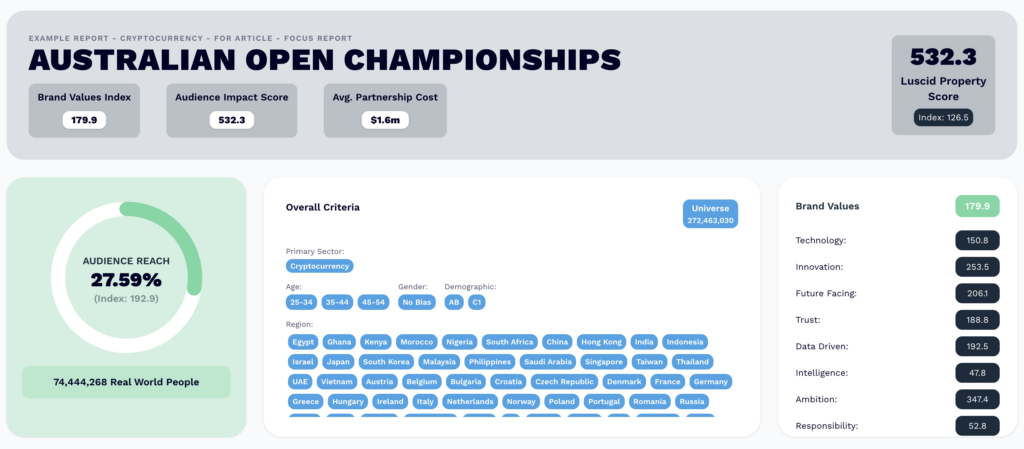

By contrast, Nexo’s partnership with the Australian Open positions the brand within a very different context. As the first crypto partner of a Grand Slam tournament, with visibility across premium hospitality spaces such as the Coaches’ Pod, the association leans toward status, global reach and a more affluent, internationally mobile audience.

The Luscid Property Focus Report highlights a leaning towards visibility and audience impact ahead of the value alignment offered by the likes of Formula 1 – for the Australian Open, 27.5% of all cryptocurrency users can be reached, which is an uplift of nearly twice the audience reach of all global individuals.

Both environments operate differently, but they serve a similar purpose. They place crypto in contexts that either intensify attention or elevate perception, depending on the nature of the audience.

The category is not tied to a single type of property. It moves across environments that reinforce different aspects of its identity, from immediacy and engagement to aspiration and premium positioning.

Photo credits: Bybit, Bitget

From financial product to cultural presence

The expansion into entertainment signals another shift.

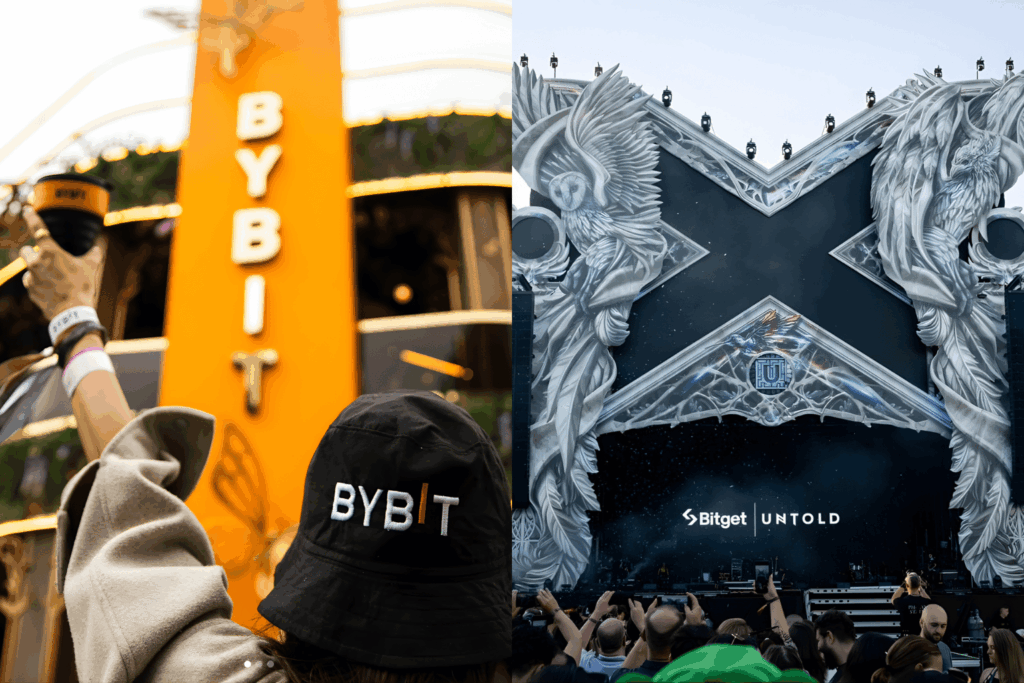

Partnerships with large-scale festivals such as Tomorrowland Brasil and UNTOLD move crypto beyond sport and into cultural space. Bybit’s role as exclusive payment partner for Tomorrowland Brasil (2025–26) integrates the brand directly into how fans access the event, with early ticket access and card-linked benefits built into the experience (PR Newswire). Bitget’s partnership with UNTOLD, reaching over 400,000 fans, positions the brand within a broader Web3 ecosystem of activations, blending digital interaction with live entertainment (Bitget).

Here, the emphasis is not just on visibility or credibility, but on integration.

Crypto becomes part of how access is granted, how payments are made, and how fans interact with events. The category begins to feel less like a standalone financial product and more like a layer within digital and physical experiences.

This is where sponsorship moves closer to behaviour. The brand is not just seen. It is used, experienced, and increasingly associated with lifestyle.

What changes when you compare environments directly

Looking across these environments reveals a more important distinction.

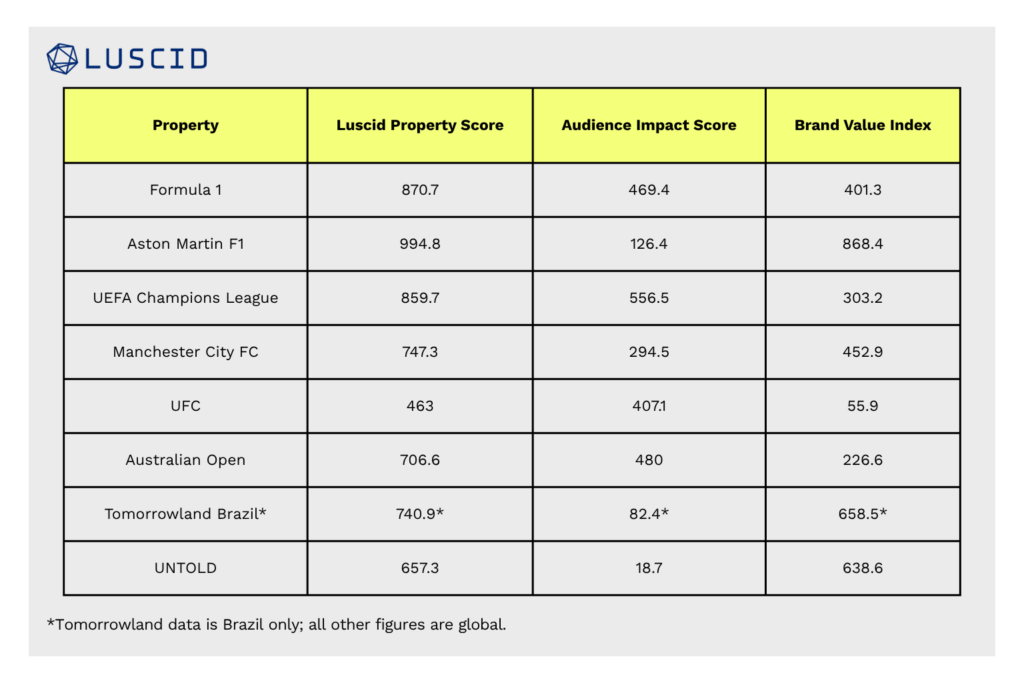

Luscid data shows that audience impact and brand value do not move together by default. Some properties generate large-scale attention but contribute relatively little to brand perception. Others, despite smaller audiences, deliver disproportionately strong brand value.

Major competitions such as the Champions League, Formula 1, and the Australian Open are highly effective at reaching large audiences. By contrast, more specific environments, such as individual teams or cultural events can generate significantly stronger associations relative to their size. At the same time, some properties sit in between, delivering strong attention but more limited brand transfer.

This distinction is critical.

It shows that sponsorship outcomes are not interchangeable. The same investment in different environments can produce entirely different results.

Reach and meaning are not the same thing.

A more precise way to think about sponsorship

Taken together, these patterns suggest that crypto sponsorship is no longer best understood as a series of individual partnerships, but as a system of complementary roles that need to be deliberately structured.

What appears on the surface as a collection of deals across different properties is, in practice, a balance between distinct outcomes. Some environments are more effective at building scale and sustained visibility, others are better suited to driving engagement and participation, while a separate group contributes more meaningfully to how a brand is perceived within the category. The difference between them is not simply one of audience size, but of function.

As a result, the most effective strategies are not built around selecting a single “right” property, but around combining environments in a way that reflects the broader objectives of the brand. Motorsport, football, combat sports and entertainment are not interchangeable choices; they are components within a wider system that, when aligned correctly, can reinforce one another.

This is where clarity becomes critical. Not only in deciding where to invest, but in defining what each partnership is expected to deliver before it begins, and how it contributes to a broader, more coherent sponsorship strategy.

Where the next opportunities may emerge

The current pattern also suggests where the category may expand next.

Some of the strongest-performing environments are not the most obvious. When measured against specific objectives, areas outside the traditional focus of crypto sponsorship begin to stand out.

Luscid data highlights this clearly. For engagement, properties such as Formula E (232.6), triathlon (187) and cycling (175.3) significantly over-index. For awareness, live events (204.5) and even sports like swimming (169.3) deliver stronger-than-expected results.

These are not the most visible platforms in the category today. But they are environments where outcomes are more precisely aligned with specific goals.

This points to a shift in how sponsorship decisions may evolve. As the market matures, brands are likely to look beyond the most prominent properties and toward those that deliver more targeted impact, whether that is engagement, reach, or relevance.

The question is no longer just where crypto fits. It is which environments are most effective for the task at hand.

Closing thought

Crypto sponsorship is not defined by the scale of the platform alone, nor by simple presence within the most visible properties, but by the way in which those environments shape how the category is perceived, interpreted, and ultimately adopted.

Across sport and entertainment, a consistent pattern continues to emerge, with crypto brands concentrating in spaces where audiences already exhibit behaviours aligned with the category, and where the surrounding context helps make crypto feel more familiar, more credible, or more relevant than it might in isolation.

What changes from one environment to another is not just the level of exposure, but the way in which the category is framed, whether through performance, routine, attention, or cultural integration, and it is this framing that increasingly determines how effectively sponsorship contributes to broader brand objectives.

As the category matures, the advantage lies not in visibility alone, but in the ability to place the brand in contexts that accelerate understanding and acceptance in a way that aligns with its intended role within the market.

Sponsorship works better with clarity.

Stay Updated with Luscid

Be the first to receive exclusive sponsorship insights, industry trends, and platform updates.