Introduction: why sponsorship matters differently in payments

Sponsorship has long played a role in how brands establish presence and familiarity. For many consumer categories, repeated exposure alone can drive preference. Payments and financial services operate under different conditions. Consumers do not actively seek out payment brands in the same way they seek out products or entertainment. Instead, payment brands are selected under pressure: when money is moving, when risk is perceived, and when failure carries immediate consequences.

As digital payments scale globally, this dynamic intensifies. According to Statista, global digital payment transaction value is projected to reach $26.9 trillion in 2026. That figure represents trillions of individual decisions carrying a quiet evaluation of reliability, safety, and confidence.

This context explains why sponsorship plays a different role for payment brands than it does for many consumer categories. The objective is less about attention and more about reassurance. Therefore, sport and entertainment matter because they are environments where emotion, trust, and behaviour intersect at scale.

The market signal: long-term investment, not short-term testing

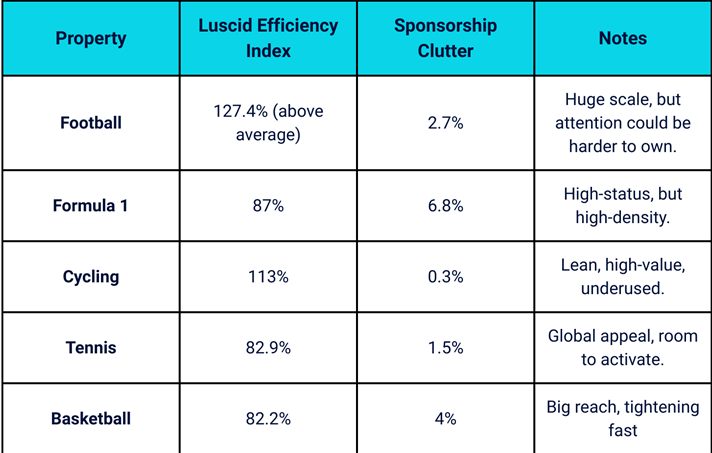

The scale and structure of current sponsorship investment make this shift visible. Payment brands collectively account for an estimated $2–3 billion in annual sports sponsorship spend, with Visa and Mastercard leading the category in both deal volume and spend (Luscid / GlobalData).

What is notable is not only the amount invested, but the nature of the commitments. These partnerships are typically multi-year, global in scope, and deeply integrated into broader brand strategies. That pattern suggests the category has moved beyond experimentation. Sponsorship is increasingly treated as a structural component of how payment brands build trust, reinforce usage, and differentiate themselves across markets.

Understanding this evolution requires looking at how different partnerships are designed to serve distinct business objectives.

Photo credits: Mastercard, Wimbledon, Global Payments

Trust and security as brand foundations

- Mastercard × McLaren Formula 1 Team

One core role sponsorship plays for payment brands is reinforcing perceptions of trust and security at global scale. The partnership between Mastercard and McLaren Formula One Team illustrates this clearly.

Estimated at approximately $100 million per year, the partnership is among the largest on the Formula One grid (Luscid). Its value lies in the environment it operates within. Formula One is defined by precision engineering, operational discipline, and risk management under pressure. These attributes align closely with the expectations consumers place on payment brands.

Data from the Luscid platform shows the partnership reaching 29 million highly targeted customers, while delivering 3.8× stronger positive association with trust and 9.3× stronger positive association with security compared to the average sports property. These metrics indicate that the partnership reinforces foundational brand signals that matter before any transaction occurs.

In this context, sponsorship functions as a reinforcement mechanism. It strengthens confidence, creating conditions where consumers feel comfortable relying on the brand across markets and situations.

Infrastructure and everyday usage

- Global Payments × Stadiums and venues

A second role sponsorship plays is operational rather than symbolic. Global Payments provides commerce and payment technology across 160+ stadiums and entertainment venues worldwide, supporting ticketing, concessions, and in-venue point-of-sale systems (Global Payments).

Live events concentrate transactions into short timeframes where speed, reliability, and ease of use directly affect the fan experience. In these settings, payment brands are remembered through performance rather than messaging.

Luscid data helps explain why this model is effective. Live Events index at 177.3 on the Luscid platform, making them 77.3% more effective than the average of 78 genres at delivering partnership outcomes for the payments sector. Additionally, 35% of Global Payments’ audience shows an active interest in Live Events, indicating strong alignment between the brand’s audience and the environment.

Here, sponsorship integrates directly into behaviour. Usage becomes habitual because the payment solution is embedded where transactions naturally occur.

Access as a differentiator

- American Express × Live sports and entertainment

A third sponsorship role focuses on differentiation through access. American Express has consistently structured its sports and entertainment partnerships around exclusive experiences, including ticket presales, reserved seating, hospitality, and cardmember-only events (American Express).

This approach shifts the value equation. The payment method itself becomes a gateway rather than a utility. Consumers choose the brand because it unlocks opportunities that are otherwise unavailable.

Luscid analysis shows where this strategy performs most strongly. When Event or Experience is the primary activation focus, Soccer, Basketball, and Tennis emerge as the most effective sports. Live Events rank first overall, with Rock Music ranking fourth, reflecting sustained demand for premium, in-person experiences.

In these environments, loyalty is driven by perceived privilege and access rather than convenience alone.

Photo credits: Angel City FC

A consistent pattern across different environments

Across these examples, a clear pattern emerges. Different properties support different business outcomes:

- Formula One creates a context where trust and reliability are reinforced while money moves across borders

- Stadiums and venues normalize everyday transactions through embedded infrastructure

- Live sports and entertainment create differentiation by linking payment methods to access

Payment brands are selecting sponsorship environments based on how they support specific objectives within the customer journey. The decision is less about audience size and more about behavioural relevance.

What sponsorship clarity reduces

This evolution has implications for risk management. Large-scale sponsorship decisions, often exceeding $10 million, carry execution, alignment, and opportunity risk. Clarity about the role each partnership is meant to play reduces uncertainty before performance metrics appear.

Knowing where trust is reinforced, when usage naturally follows, and which environments align with audience behaviour allows payment brands to structure partnerships more deliberately. The result is greater strategic coherence across markets and channels.

Conclusion: the next frontier

Sponsorship in payments is increasingly defined by purpose rather than presence. The next phase is shaped by environments where consumers feel confident relying on a brand when it matters most.

For payment brands operating at global scale, success depends on choosing partnerships that reinforce trust, support habitual usage, or unlock access in ways that align with their broader strategy.

Sponsorship works better with clarity.